Menu

Lending Facilities - Merchant Cash Advance, Factoring Facilities & Revenue-Based Financing

September 21st, 2022

Merchant Cash Advances

A merchant cash advance is a type of loan that offers a cash advance against future sales. The term is commonly used to describe a variety of small business financing options, providing quick cash for business. A merchant cash advance provides alternative financing to a traditional small-business loan. Under this arrangement, a lump-sum payment is made from the lender to businesses and the businesses then pay it back as they make sales to customers. It has been historically used largely by businesses whose revenue comes primarily from credit and debit card sales. Businesses in need of capital and with a steady volume of credit card sales (including, retail stores, restaurants, and salons and auto repair shops) are among the companies most likely to avail themselves of this kind of financing.

Obtaining a merchant cash advance is usually a simple process. After an application has been made an approved, the lump-sum payment can be collected within a few business days of the application. A merchant cash advance provides anything from a few thousand dollars to over $200,000. However, the payback period is usually short — 18 months or less, in most cases. Instead of one fixed monthly payment from a bank account over a predetermined repayment period, businesses make regular or weekly payments, plus fees, until the advance is paid in full.

The repayment of a merchant cash advance can be achieved in two ways: (a) an upfront cash payment in return for a percentage of potential credit and debit card sales, or (b) an upfront cash payment that is repaid by remitting fixed regular or weekly debits from the bank account, known as ACH (Automated Clearing House) withdrawals. According to Sean Murray, a former merchant cash advance broker and founder of trade publication deBanked, the latter (ACH merchant cash advances) has become the most popular type of merchant cash advance and lets providers market to companies that are not solely focused on credit and debit card sales.

The borrower’s ability to repay the merchant cash advance determines how much they will pay in fees. When expressed as an APR, the cost may be substantial — often much more so than other forms of business loans. Merchant cash advance lenders charge the highest rates of interest, fees and other charges, as a result a merchant cash advance can result in an APR as high as 350%. Merchant cash advances are based on two factors - the “retrieval rate” and a “factor rate.” The retrieval rate is the amount that is deducted from the business’ daily debit and credit card sales. These typically vary from 15% to 25%. Retrieval rates are often negotiated by merchant cash advance providers to make sure that the business has enough remaining revenue to be able to sustain daily operations. The factor rate commonly ranges between 1.2 to 1.4. The higher the factor rate the higher the total fees one pays in exchange for the financing. These rates are applied to merchant cash advances to measure the total cost of the loan. The cash advance is multiplied by the factor rate to arrive at the total repayment amount. For example, a merchant cash advance of $25,000 with a factor rate of 1.25 would mean a total repayment cost of $31,250. The cost of the loan then would be $6,250. Since most merchant cash advances are short-term loans, however, the APR will be much higher than a conventional, long-term loan. Higher APRs result from the combination of a higher retrieval rate (creating faster repayment) and a higher factor rate (resulting in more costly repayment).

Given the low threshold for approval, which is tied to a merchant cash advance’s higher cost of funds, a merchant cash advance could be a viable choice for businesses in need of cash quickly. It is important to know that a merchant cash advance will almost always have a higher cost of capital as a bank loan. A bank loan or line of credit could be a better choice than a merchant cash advance for those with good credit, high sales and at least two years in business.

Merchant cash advances offer a great deal of flexibility. The funds are free to be used as one sees fit, and there are a variety of payment options. For example, if a repayment plan is based on a percentage of regular sales, there is no need to pay as much when sales are poor. This is particularly useful for companies whose sales fluctuate, such as retailers that rely on seasonal sales. Another advantage of this form of financing is that borrowers can typically get their money quickly — in as little as a one or two business days. Furthermore, a prospective borrower’s credit history is less important than its sales history given that the merchant cash advance is repaid through sales (so the repayment profile is similar to a royalty). If the borrower can prove that they have had a minimum amount of credit or debit card transactions in the previous years, they are likely to qualify for a merchant cash advance. These loans are unsecured, which means no current assets need to be put up as collateral. This can be a significant benefit for businesses with limited assets.

On the other hand, a merchant cash advance is much more costly than other forms of financing. Factor rates, not interest rates, are almost always used to describe costs. A factor rate is distinct from a principal repayment schedule and interest rate in that it is not bound to a fixed time frame. Paying off the advance quicker generally will not result in savings to the borrower. Perhaps the biggest drawback of a merchant cash advance is that a part of the business’ future sales will be used to repay the advance and related costs. The gross margin profile of future sales may be lower than anticipated. Repayment from these sales, however, will still be owed — typically, on a daily basis. This can lead to cash flow issues, forcing the business to go further into debt and borrow again.

Factoring

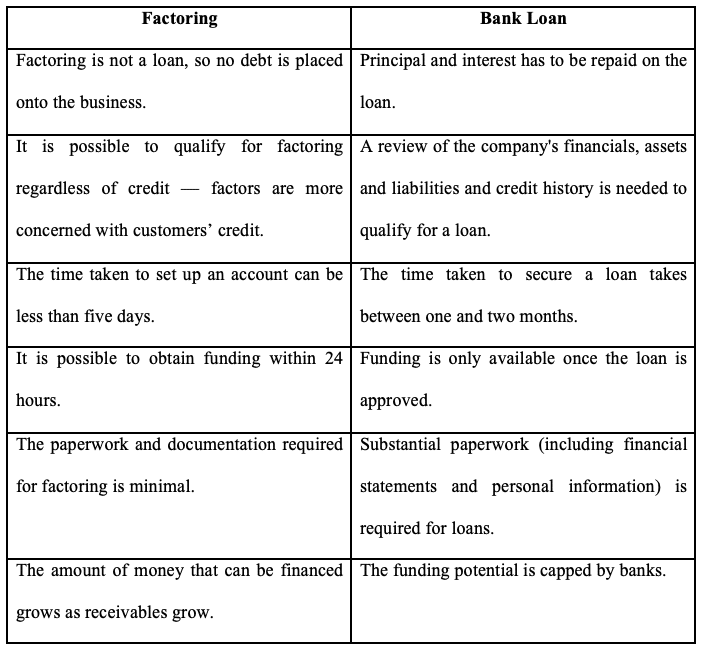

In another form of financing, often termed as accounts receivable funding, businesses may use invoice factoring to finance their cash flow by selling their invoices to a third party (a factor or factoring company). The business then normally receives payment for such invoices within 24 hours. The factoring company then receives payment from the business’ customers on those invoices. This form of financing can be contrasted with reverse factoring, also known as supply chain financing, wherein the supplier receives finance in relation to their receivables. Contrary to traditional factoring where the supplier wants to finance their receivables, in reverse factoring is a process started by the ordering company.

The primary incentive for businesses to factor is to get paid on their invoices as soon as possible, rather than waiting 30, 60, 90 or even longer for a customer to pay. The extent a company factors its invoices can be determined by their specific business requirements. Some businesses factor all of their invoices, while others factor only certain invoices such as those of consumers who have a history of paying late. Factoring provides businesses with the faster cash flow they need to pay staff, manage customer orders and expand their company. This facility essentially provides faster liquidity to the client that would otherwise stay trapped within the business’ accounts receivable. Although factoring transactions may behave similarly to a loan or other financing transaction, they are in fact as a true sale of the business’ receivables. A purchase and sale agreement is used by the finance company to purchase each invoice. The finance firm notifies the payer of the purchase and verifies the invoice’s accuracy as part of the purchasing process.

The factoring company enters into an arrangement with the business client to handle their sales ledger and credit control on an ongoing basis for a set period of time (the term of the factoring contract, typically 24 months). When a business client sends an invoice to a customer, the factoring company advances some funds upfront, usually 70-85 percent. When the end customer pays, the factoring company collects the debt and leaves the remaining balance, minus their fees, available to the business client.

Factoring is used by companies of all types, from sole proprietorships to Fortune 500 firms, to maximize cash flow. Trucking, shipping, engineering, government procurement, textiles, oilfield facilities, health care, staffing and other sectors all use factoring. Many businesses use factoring cash to pay for inventory and purchase new equipment, employ more people, increase operations or cover any other business operational costs.

The factoring company makes money through the factoring fees for each invoice and the discount assigned to each invoice by the factor. Different factors maintain different fee structures. Some factoring companies only charge an overall factoring fee based on the monthly amount of invoices submitted and discount the receivables by the creditworthiness of the payers of the invoices and the expected time until repayment. Additional fees may be required by certain factoring companies to cover money transfers, collateral and other operating costs.

Recourse and non-recourse factoring are the two major forms of factoring. Under recourse factoring, if the factoring company is unable to receive payment from the payer (the factoring customer's client), the factoring customer would become responsible for the payment of the invoice. Under recourse factoring, a factoring customer becomes a guarantor of his client’s repayment. Non-recourse factoring entails the factoring company taking on the credit risk associated with processing an invoice. Some factoring companies offer both recourse and non-recourse funding. Non-recourse factoring, which has a higher discount on the face value of the receivable, also typically have tighter limitations on the receivables that may be factored.

Factoring firms will release funds locked up in unpaid invoices for fees and discounts on the face value of the receivables, allowing the company to collect funds without having to wait for customers to pay. Factoring companies can better handle their cash flow as a result of this acceleration in payment. Many factoring firms will also handle credit management for an additional fee, which means the factoring firms will contact delinquent clients for invoice payment, which can save the factoring customer both time and resources.

Conversely, most factoring companies bind their customers to a long contract under which they must exclusively finance all of their sales ledger through the factoring facility, which can be challenging to terminate. Many invoice factoring companies can quote low prices and fees at first, but adding additional fees (or "disbursements") may add significant expense and complexity to such arrangements. Many factoring facilities are often unsuitable for companies with just one or two big customers. Factoring firms impose low "concentration restrictions" as customer diversification substantially reduces non-payment risk. Invoice caps for export operations are often imposed by international customers. Many business clients prefer to retain their own credit management rather than rely on a factoring facility to chase down payments from their customers given that these arrangements can substantially increase the fees for the facility. Furthermore, small businesses often place a premium on maintaining safe and friendly relationships with their customers rather than turn collections efforts over to factoring companies.

Revenue-Based Financing

Revenue-Based Financing (RBF), sometimes referred to as royalty-based financing, is a form of loan in which the repayments are based on a percentage of the borrower's monthly income rather than a fixed sum. It is a type of small business loan. Payments are adjusted in response to the borrower's financial performance, rising when revenue is high and declining when revenue is poor. RBF started as a source of debt funding in the oil, gas and mineral industries. It then branched out into the life sciences industry and other segments of the energy industry — including, clean technology. It has developed into other technology and non-technology fields in recent years.

RBF can be organized in a variety of ways. A term loan is the most common structure. The entire sum is usually not advanced up front. The drawdown can be spread out over several years to avoid incurring interest costs before the funds are needed. Payments (principal and interest included) are calculated using a fixed percentage of sales or cash receipts from the previous month or quarter. The structure is flexible; payments are usually made before one of the following thresholds is met: the lender receives a pre-determined multiple of the original loan; the lender reaches a pre-determined internal rate of return (IRR); or a terminal date is reached. After these thresholds are met, the loan obligation expires and no further payments are due.

Unlike several other types of lending, revenue-based financing is specifically the debt to be paid off over time. If properly structured, repaying debt with revenue-based financing can be much more manageable than with other funding solutions because of the monthly payments. Similarly structured debt funding, such as merchant cash advances, follow the same percentage-based repayment arrangement, but involve daily repayments instead of monthly repayments. Revenue-based financing thus affords a more manageable product to repay. Furthermore, as opposed to other types of financing, revenue-based financing provides much greater amounts of money. Using merchant cash advances for example, borrowers can only expect to receive up to $250,000. With revenue-based financing, minimum sums of $100,000 to $2 million are often available, with some companies offering even more.

Finally, unlike conventional types of financing, there is no need for excellent personal credit or a long track record in business to be qualified for revenue-based financing. Over the last five years, revenue-based financing has become increasingly common because many for emerging growth companies are unable to obtain traditional business loans. Revenue-based financing is therefore ideal for growing businesses that cannot get traditional financing because of their credit or length of time in business, if such companies have a substantial sales and growth potential. Revenue-based Lenders may also provide greater loan amounts and less restrictive covenants than banks, which are subject to significantly higher regulatory burdens.

Conversely, one major downside of revenue-based financing is the cost of capital may very high (although revenue-based financing tends to have a lower cost of capital than merchant cash advances on an APR and IRR basis). Revenue-based financing is a long-term version of merchant financing; as a result, revenue-based financing requires very high factor rates for each credit obligation. Revenue-based financing is also relatively slow to fund. Most firms offer a 30-day turnaround, which is slower than firms providing financing through merchant cash advances. Lastly, while revenue-based financing is more available to emerging growth companies because it does not require conventional loan qualifications, a business still must meet certain criteria to be eligible for this form of financing. The business will need to have detailed sales and growth forecasts and a detailed budget, which for a new business may be difficult to create or keep up to date.

References:

(1) Blakeney, J. (2020). Merchant Cash Advances vs. Invoice Factoring. Retrieved from https://arfunding.com/industry-news/merchant-cash-advances-vs-invoice-factoring/

(2) Nicastro, S. (2020). Is a Merchant Cash Advance Right For Your Business? Retrieved from https://www.nerdwallet.com/article/small-business/merchant-cash-advance

(3) Commercial Capital LLC. Typical Factoring Rates. Retrieved from https://www.comcapfactoring.com/blog/average-factoring-costs/

(4) Fora Financial (2019). Four Industries that Benefit from Merchant Cash Advances. Retrieved from https://www.forafinancial.com/blog/working-capital/four-industries-benefit-merchant-cash-advances/

(5) CGF Merchant Solutions (2019). Will Revenue Based Funding Replace the Merchant Cash Advance? Retrieved from https://cfgmerchantsolutions.com/revenue-based-funding-merchant-cash-advance/ hhttps://cfgmerchantsolutions.com/revenue-based-funding-merchant-cash-advance/

(6) RTS. What Is Factoring? Retrieved from https://www.rtsinc.com/guides/what-factoring#

(7) Riviera Finance (2020). Factoring: How Do They Compare? Retrieved from https://www.rivierafinance.com/finance-blog/merchant-cash-advances-vs-invoice-factoring-how-do-they-compare/

(8) Detweiler, G. (2020). What Is a Merchant Cash Advance? Retrieved from https://www.thebalancesmb.com/what-is-a-merchant-cash-advance-4687173

(9) Market Finance. Factoring Explained. Retrieved from https://marketfinance.com/business-finance/what-is-factoring

(10) Commercial Capital LLC. Asset Based Lending vs. Factoring. Retrieved from https://www.comcapfactoring.com/blog/asset-based-lending-factoring/

(11) Wood, M. (2020). Revenue-Based Financing: Everything You Need to Know. Retrieved from https://www.fundera.com/business-loans/guides/revenue-based-financing

(12) Find Venture Debt. Revenue-Based Financing. Retrieved from https://www.findventuredebt.com/types-of-venture-debt/revenue-based-financing

(13) Trade Finance Global. Reverse Factoring. Retrieved from https://www.tradefinanceglobal.com/finance-products/reverse-factoring/

Categories: News